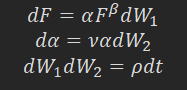

SABR Hagan近似では条件によっては確率密度がマイナスとなり、無裁定が保証されないことが知られている。ここでは実際に裁定可能となるケースを試行する。

通貨オプションEUR/USDテナー10Yフォワードレート1の場合、Table 1のパラメータでFDMとHagan近似を実行するとFigure 1の様に、10d Put, 25d Put, ATM, 25d Call, 10d Call の値(Table 2)は"ほぼ"一致する(FDMとDNN近似も"ほぼ"一致するが,ここではより正確なFDMの値を使用)。

It is known that under certain conditions, the probability density in the SABR

Hagan approximation can become negative, failing to guarantee arbitrage. Here,

we test cases where arbitrage is actually possible.

For the EUR/USD currency option with a 10-year tenor and a forward rate of 1, executing FDM and Hagan approximations using the parameters in Table 1 yields

results as shown in Figure 1. The values for the 10-day Put, 25-day Put, ATM, 25d Call, and 10d Call (Table 2) are "nearly" consistent (FDM and DNN approximations also show "nearly" consistent results, but the more accurate FDM values are used here).

| α | β | ρ | ν | |

|---|---|---|---|---|

| FDM | 0.12 | 0.7 | -0.3 | 1.2 |

| Hagan | 0.08044142 | 0.5553495 | -0.1524933 | 0.461517 |

|

||||

| strike | Vol | |

| 10d P | 0.5677937 | 0.1795065 |

| 25d P | 0.8331094 | 0.1181222 |

| ATM | 1.041572 | 0.0898553 |

| 25d C | 1.353767 | 0.1124491 |

| 10d C | 2.355184 | 0.1740777 |

Figure 1 Volatility Curve

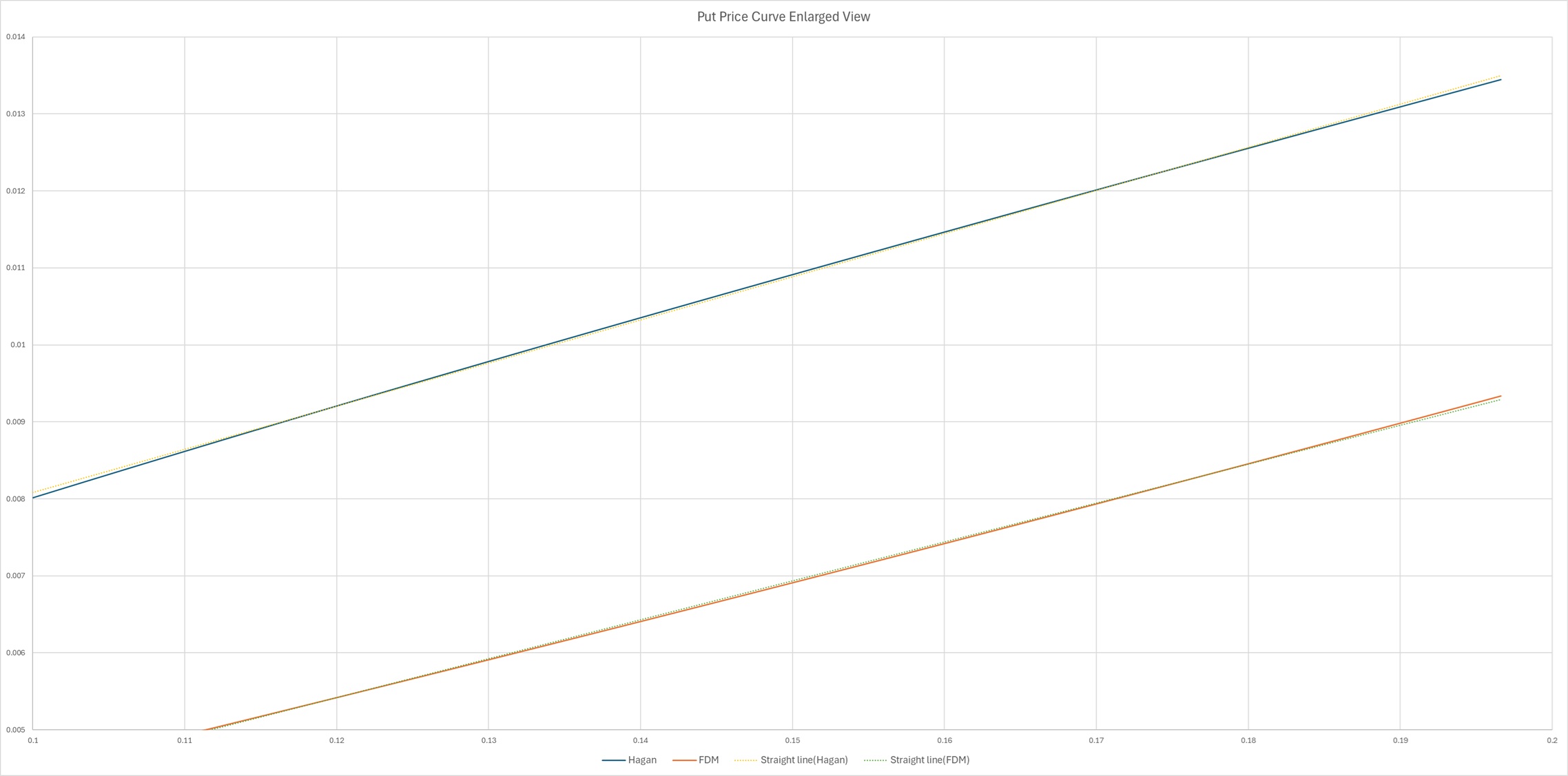

このケースのオプション価格と行使価格の関係は、Figure 2のようになるが、Hagan近似の場合、ストライクが0.5以下では凸関数となっている。凸となっている部分では裁定取引が可能。

The relationship between the option price and strike price in this case is as shown in Figure 2. However, in the Hagan approximation, the function is convex when the strike is 0.5 or less. Arbitrage is possible in the convex portion.

Figure 2 FX Option Price Curve